SensingSG Q1 2026 Briefing: Singaporeans Back National Direction even as Personal Finance Sentiment Diminishes

Despite Recent Government Support, Doubling of Economic Pessimism Suggests Global Price Hikes are Starting to Hit Home

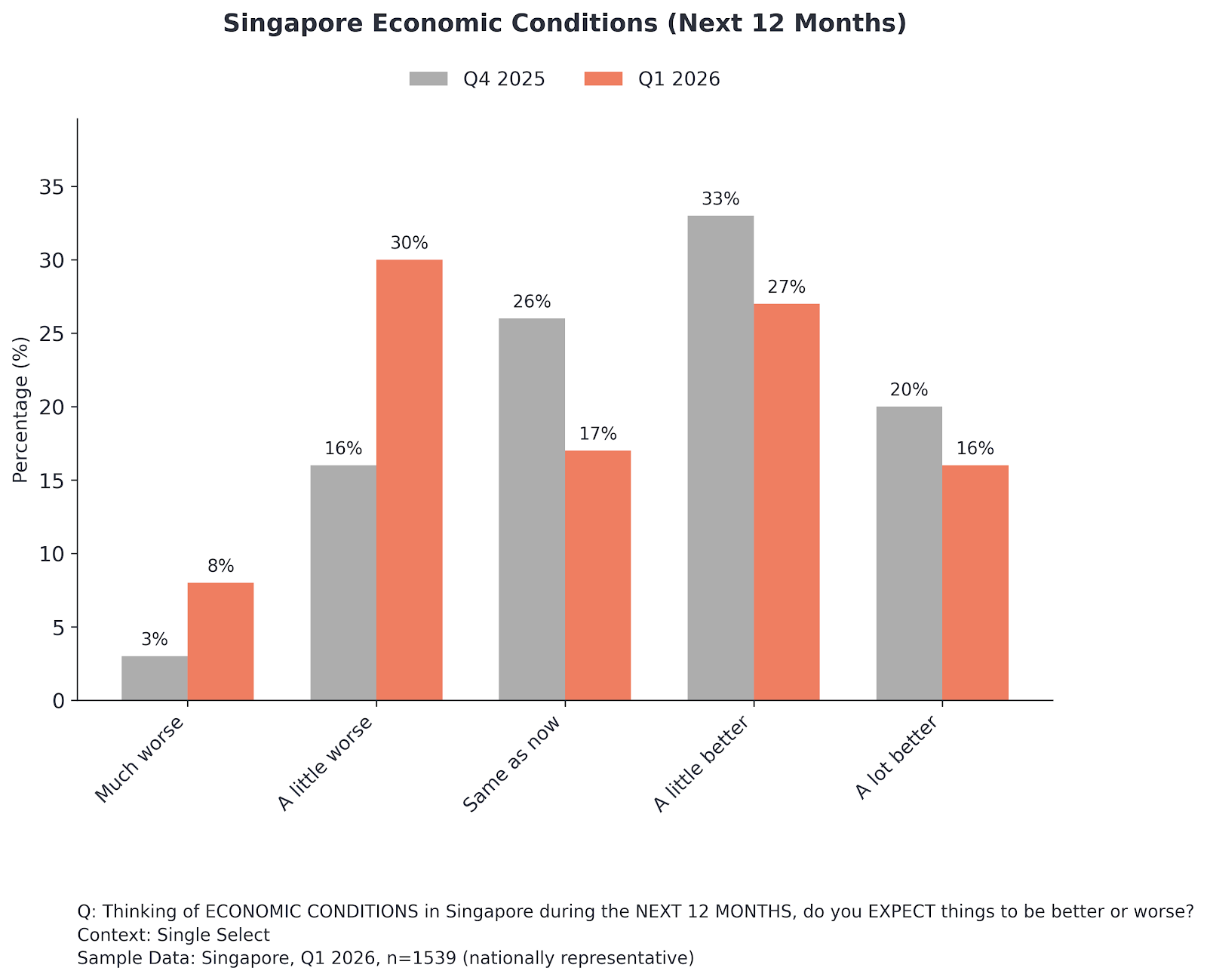

Singapore currently maintains a high trust equilibrium that masks a significant deterioration in household economic sentiment, according to the latest findings from SensingSG, Blackbox Research’s quarterly sentiment tracker. While 89% of citizens believe the country is headed in the right direction, economic pessimism has doubled in a single quarter, with two-in-five (38%) locals now expecting economic conditions to worsen in Singapore.

The Iran War and the Oil Filter

The primary driver of this shift is external. The Iran war and the subsequent surge in oil prices past US$100 have moved from being a geopolitical headline to a topline household concern. Our intelligence indicates that these external shocks are now a primary consideration for Singaporeans when assessing their future.

Economic pessimism has doubled in a single quarter. In Q4 2025, only 19% of respondents expected conditions to worsen in the next 12 months; today, that figure stands at 38%. This "anticipatory anxiety" is directly linked to energy security concerns, which are now filtering through to every facet of the domestic economy.

An Erosion of Economic Sentiment

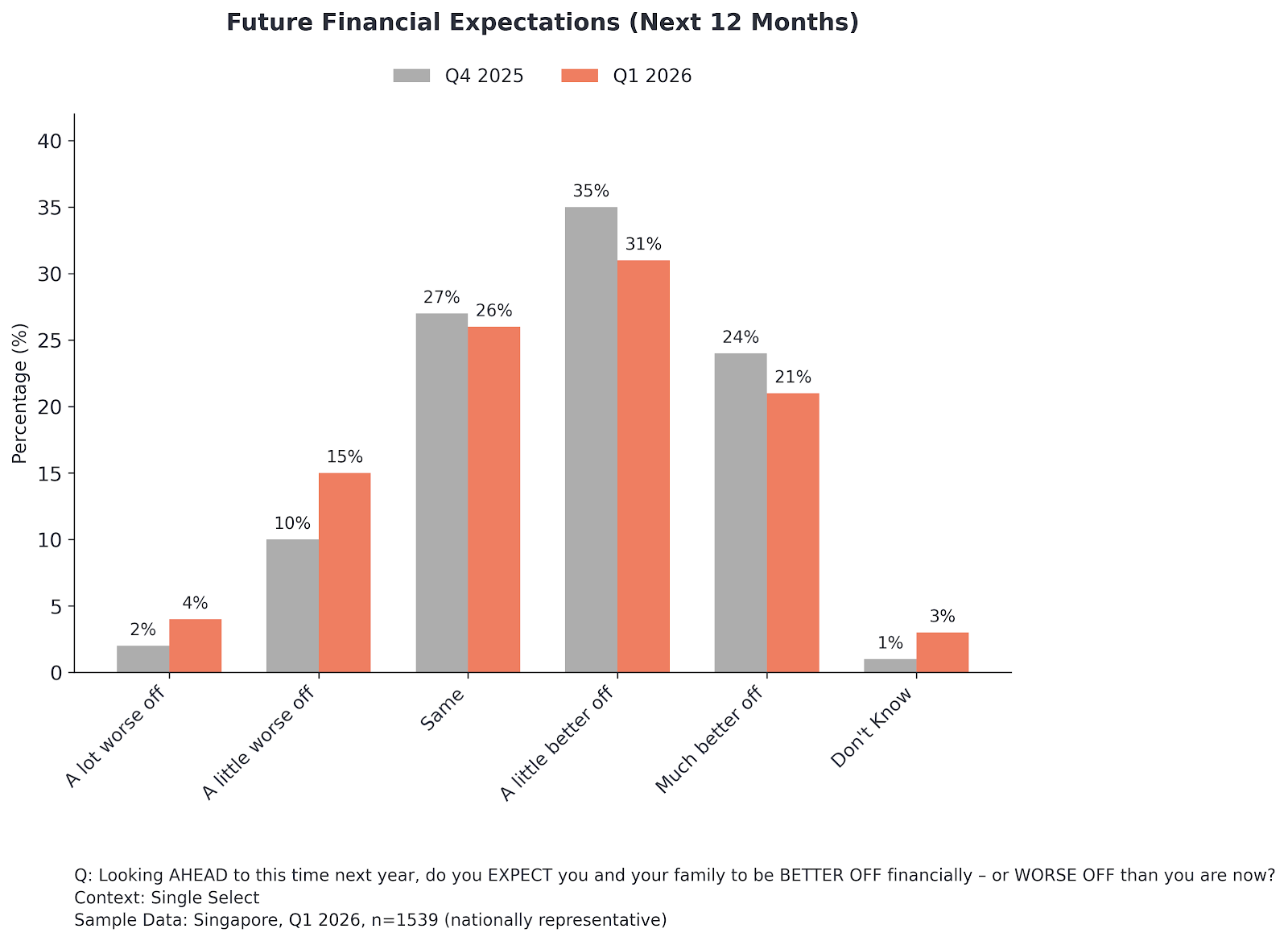

A striking data point in this quarter’s briefing is the erosion of personal financial sentiment. The proportion of families feeling "better off than a year ago" has dropped from 54% in the previous quarter to just 46%—the lowest reading Blackbox has recorded in two years.

Despite the positive reception of the February Budget, the "Budget Glow" has been extinguished by the reality of the pump and the utility bill. Nearly one-in-five Singaporeans (19%) now expect to be financially worse off this time next year, a 6-point jump that reflects a growing sense of vulnerability.

Sectoral Performance: Notice for Policymakers

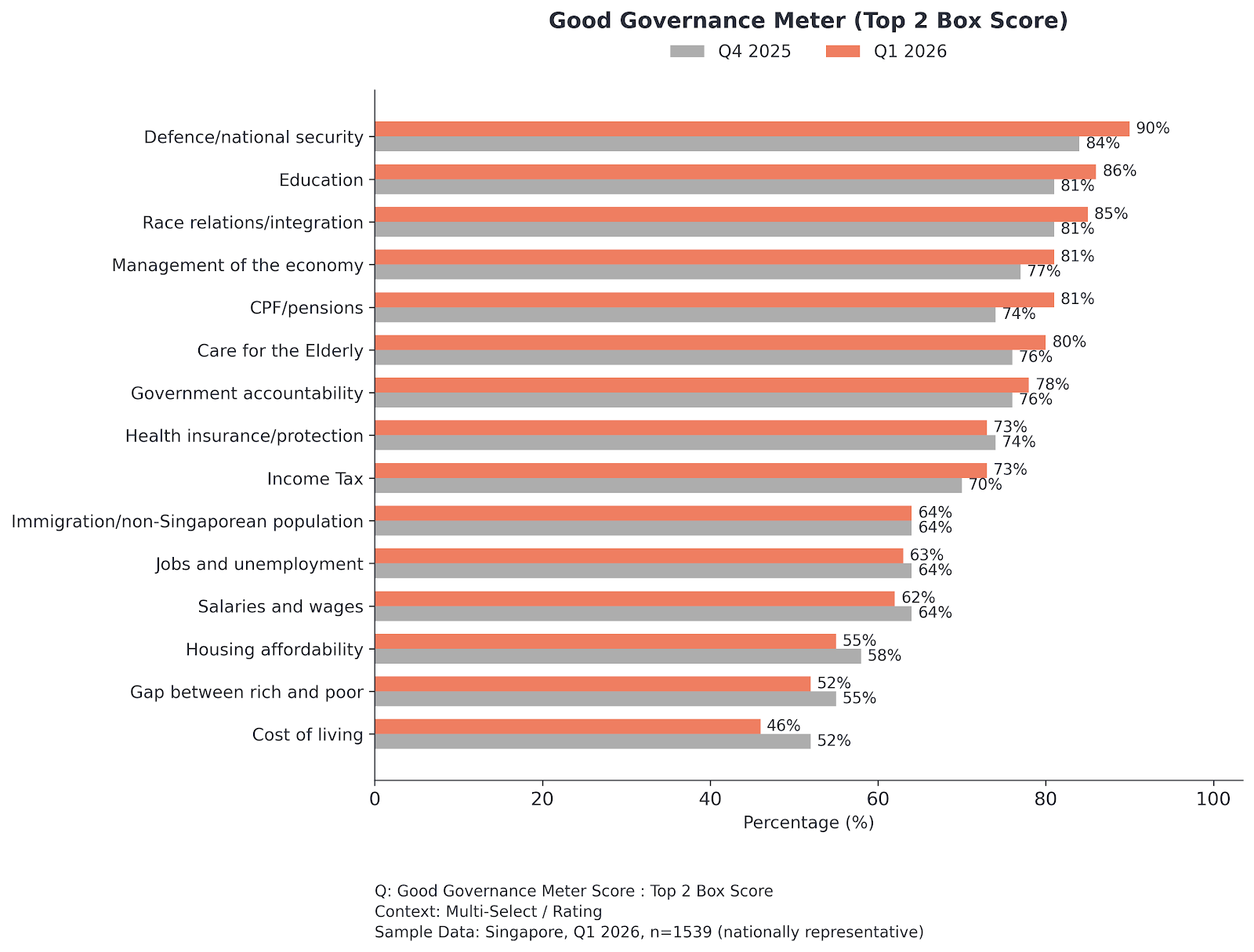

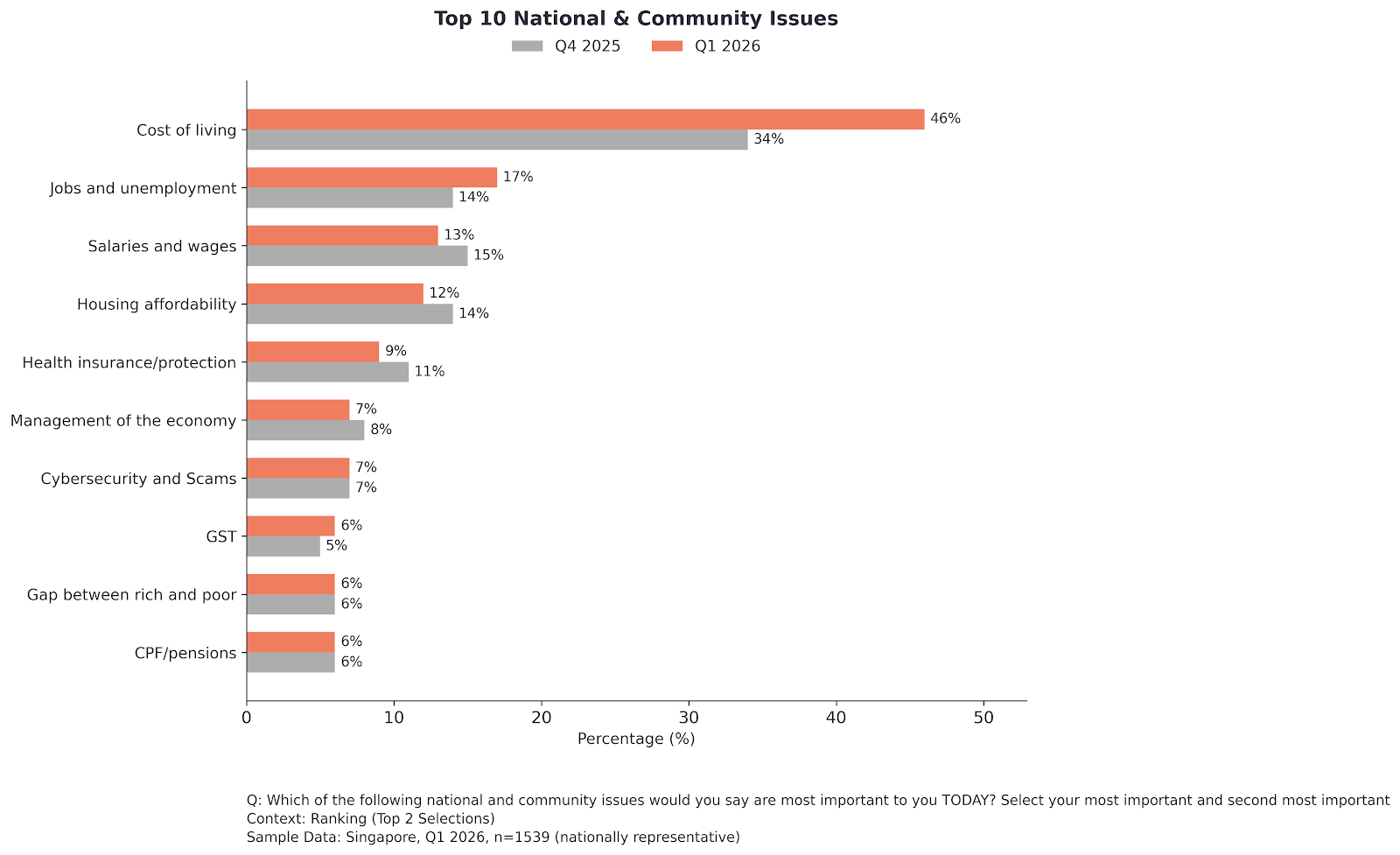

While the Government receives high marks for Defence and National Security (+6pts)—likely a reaction to the global geopolitical climate and erratic behaviour of governments overseas—ratings for economic management are lessening. The Government’s performance on "Cost of Living" has slipped 6 points to 46%, while other key measures such as housing affordability, the wealth gap, and GST have all declined by at least 3 percentage points.

This suggests that while the social impact remains intact regarding issues like national security, the public is increasingly looking for more aggressive intervention on bread and butter issues. Cost of Living is now the undisputed number one concern for the population, seeing a significant quarter-on-quarter increase.

Strategic Implications

For the C-Suite: Navigating the Defensive Consumer

The Flight to Value: Families will likely tighten discretionary spending as they recalibrate for energy costs; brands should pivot messaging toward resilience and reliability.

The Transparency Mandate: Energy-sensitive sectors must offer clear pricing transparency to avoid "corporate greed" accusations amidst US$100 oil.

Employer Value Proposition: As personal finances slip, employees will prioritise cost-of-living support and flexible work to mitigate rising commuting expenses.

For Policymakers: Bridging the Stewardship Gap

The Handout Paradox: Falling satisfaction with living costs (46%) indicates the public now views budget handouts as "temporary patches" rather than structural fixes.

Leveraging Security Trust: Strong trust in National Security (+6pts) allows the energy transition to be framed as a strategic necessity rather than mere fiscal management.

Addressing "Hidden" Declines: Declining sentiment on GST and housing reveals "bread and butter" risks that could undermine institutional support during a downturn.

Conclusion: Trust is a Buffer, Not a Solution

Singapore enters the middle of 2026 in a position of institutional strength, but the data tells us that trust is being used as a shock absorber for economic pain. Even the "stewardship premium" of Singapore’s established good governance and public trust has limits.

For both the boardroom and the cabinet, the next 90 days will be critical. The high "Right Direction" score should not be taken merely a sign of contentment—it is a mandate for proactive intervention before the anticipatory anxiety of Q1 becomes the economic reality of Q2.

Blackbox is Asia’s leading provider of decision intelligence. Reach out to us to find out how our holistic range of market research solutions can help your organisation make decisions that matter.